Transmission, Transition, and Transactions: The Energy Surge & What it Means for M&A

By: Eric Lohmeier, CFA and Ryan Goetzinger, CFA

As the AI boom accelerates demand for energy, utility services have become one of the most resilient and investable sectors in the current M&A environment. The next five years are likely “game on” for energy infrastructure buildout, but selectivity and underwriting rigor remain key.

Key Takeaways

- Aging infrastructure, AI-driven load demand, and federal policy support are accelerating grid investment. Utilities are leaning heavily on outsourced service providers to meet urgent electrification, modernization, and generation growth goals.

- Valuations in AI-adjacent sectors are inflated, infrastructure buildouts face labor and equipment bottlenecks, and policy shifts have created regulatory uncertainty.

- The utility services sector offers strong long-term fundamentals tied to electrification and grid hardening, but AI-driven theses will not generate returns commensurate with current valuations, as the hype has created a clear bubble. Investor returns will depend on disciplined selection, thoughtful timing, and a clear view of where hype ends and durable demand begins.

Over the past several years, the energy ecosystem has changed faster and more dramatically than most investors expected. Our team has dedicated substantial time and resources into understanding how energy utilities will evolve and which service providers they will rely on to satisfy increasing demand. Infrastructure services have always been a core focus of our firm, and we’ve accumulated experience navigating this space from early federal incentives, to AI’s sudden impact on load forecasts, and through the current flood of inbound investor interest. Our team has advised on transactions representing over $1 billion in our infrastructure vertical in the last 5 years alone. Most recently, NCP advised Vannguard Utility Partners on its sale to Trivest, and we wanted to share our insights with our friends and partners. In addition, for over a decade, NCP has been a core M&A partner with Wright Service Corp, one of the largest utility environmental companies in North America.

Looking ahead, we believe the next several years will continue to be defined by electrification, outsourcing, and a scramble for capacity, but not all opportunities are created equal. Projects and platforms that look attractive today may underperform if political winds shift or demand forecasts fall short. We remain focused on diligencing the next wave of acquisition targets that are positioned to thrive, even if the next chapter looks different than today’s.

Energy Infrastructure Today & Tomorrow

US infrastructure at-large has been increasingly in need of improvements – the electric and gas infrastructure is pushing 40-50 years, well past this equipment’s intended useful life. The US has a D+ grade on energy infrastructure1, and relying solely on funds from the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA) isn’t going to fully close the gap. Another upcoming capacity challenge is that while total electricity generation in the last 25 years in the US has only grown marginally, the increasing electrification of our daily lives is creating conditions for a significant uptick in load. With the rise in electric vehicle (EV) usage, proliferation of data centers, and federal/state emissions goals, utilities will need to double transmission capacity to connect new energy sources2. While the momentum for EVs and reducing greenhouse gas emissions has declined in the past year, we believe these trends will ultimately continue to drive the market long-term. In addition, given that renewable energy sources, specifically solar, have proven to be the lowest incremental cost energy sources, further buildout of infrastructure for these sources will continue.

In addition to growing capacity, utilities are also focusing on resilience to ensure current/new infrastructure can withstand the variety of threats faced today. The vast majority of power outages are caused by severe weather, and utilities are combating this with a variety of approaches, including undergrounding power lines and smart grid technologies. Also, with intermittent generation sources (e.g., solar and wind) taking up more market share, utilities are navigating methods to ensure customers have reliable service. Recent advances in battery technology are assisting these efforts, as batteries have the potential to unlock a more flexible and cost-efficient grid.

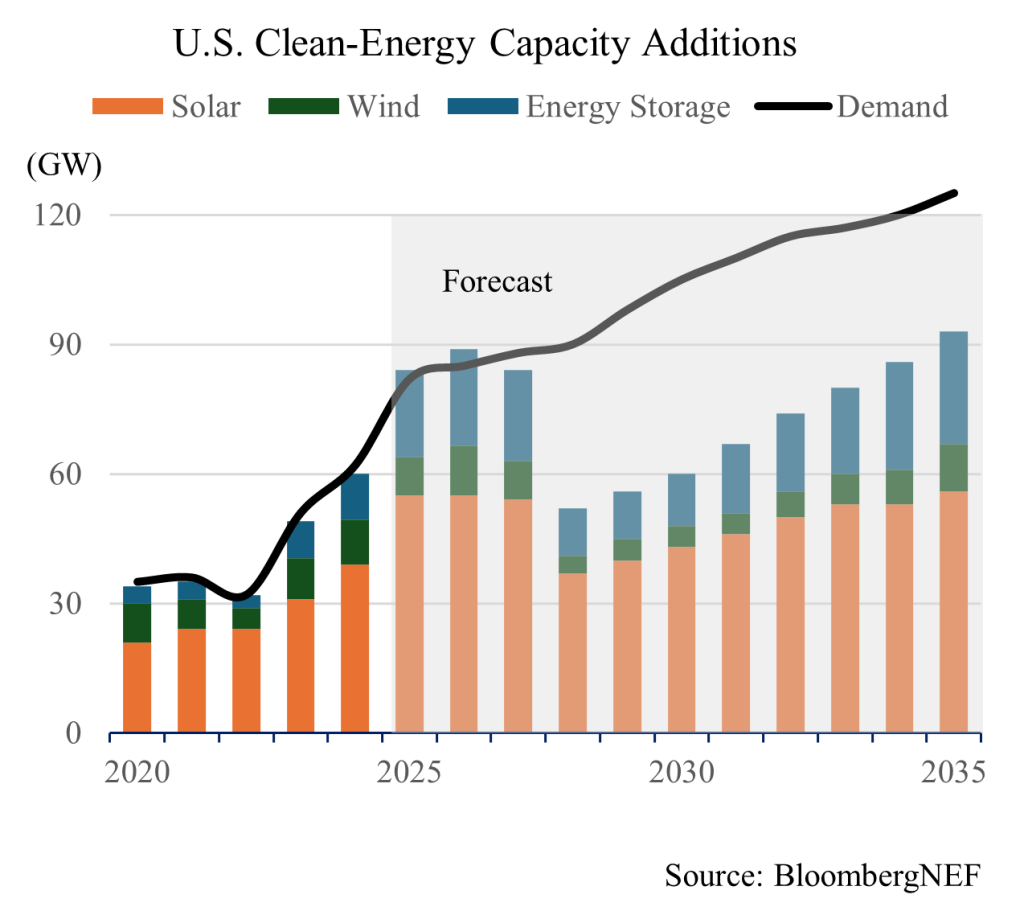

Policy is playing a critical role here, too. The One Big Beautiful Bill Act (OBBB) has continued many of the funding mechanisms from IIJA and IRA, while also beginning efforts to streamline permitting and expand access to federal land for natural gas projects. Wind and solar incentives remain through 2027–2028, creating a race to begin projects before the window closes. Nuclear and geothermal credits also survived, which has fueled a rush to scale these technologies. In addition, with the reduced emphasis on emissions, coal generation becomes viable again. Even though the long-term rules of the road may not be explicitly clear, specifically on renewable energy sources, it appears all generation sources are set to scale significantly to meet demand growth. For renewable energy sources, the question marks come into play following the sunsetting of incentives (Figure 1), but with the challenges to nuclear (lengthy timelines) and natural gas (turbine production capacity), renewables appear to be a compelling option to ramp up capacity quickly. However, renewable projects also contain significant risk today with legislative and regulatory challenges.

Accelerating Investment aka AI

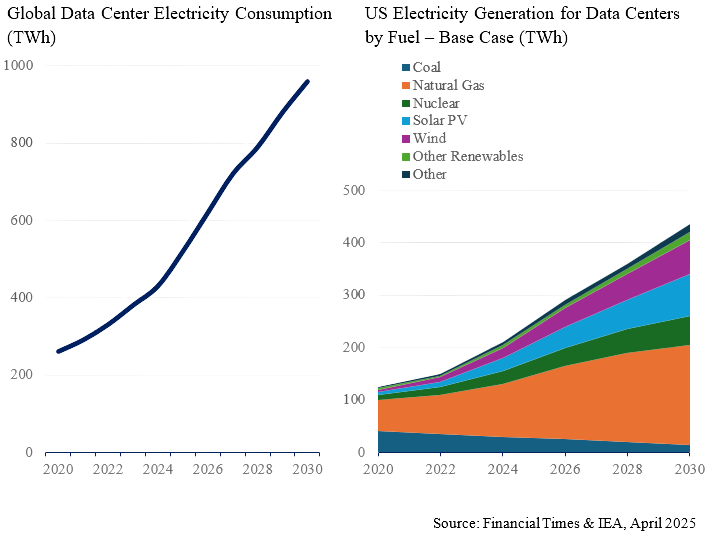

The trillions being spent to ramp up computing capacity to facilitate LLMs and inference dominates the news cycle, but the accompanying resource drain receives less attention. In order to accommodate AI’s energy appetite (Figure 2), energy production, storage and transmission need major investments. Utilities have been moving toward an outsourced model for many years, but given the time crunch in ramping up capacity, AI demand further accelerates the need to outsource key functions to high quality service providers. Given the aggressive valuation assumptions of AI companies, there will be numerous groups and mega tons of money invested to reduce the likelihood that energy capacity is not a limiting factor.

Energy prices have increased faster than inflation since 2022 (13%)3, which is partially attributed to the consumption jump driven by AI. We can expect utilities to exert pricing power, which therefore improves pricing power for service providers. However, increases in energy prices also invites more consumer and policy scrutiny as consumers have to dedicate more of their wallet to what is today an essential utility.

The AI bubble has been covered ad nauseum, with many venture capitalists fully admitting there is a bubble taking place. While AI progress could meaningfully disrupt every industry and create trillions in wealth, as many folks in Silicon Valley are predicting, our bet is that the returns within AI will not be commensurate with the capital being deployed today. Therefore, even though the timing and severity of the pullback in AI capital expenditures is uncertain, we do not believe the current pace of investment is sustainable without a proven business model. If and as this is scaled back materially, there are downstream effects, specifically a reduction in the projected load demand.

What Could Pull the Plug on AI?

The Silicon Valley mindset with AI has been something like: don’t worry about the negative externalities associated with building LLMs, AI will create so much productivity that it will outweigh any negative effects. While that may turn out to be the case, the voices pushing back against those negative externalities are getting louder. Other energy consumers are becoming more concerned the strain on utility infrastructure will raise energy costs across the board. In addition, with the cooling needs of data centers, water infrastructure is also under strain.

Will communities be comfortable taking on certain negative effects in exchange for possible positive effects that would primarily flow to Silicon Valley? Tech companies have historically sold communities on the economic benefits of data centers, but elected officials and citizens are waking up to the fact that construction is the only material area in which a community benefits, which is temporary and creates effectively zero long-term value. Therefore, the days of hyperscalers receiving generous incentive packages are numbered, and these companies are already shifting to dedicated generation sources on new data centers to limit grid disruption.

On the energy needed to power data centers, further bottlenecks on products and labor are likely to continue. Overall, we believe continued uncertainty on US tariff policy will make costing of these projects difficult and create supply chain challenges. Specifically on the product side, transformers and gas turbines are seeing a major supply crunch that will take several years to work through. In addition, China dominates the market for solar panels and batteries, so these projects carry major supply chain uncertainty. On the labor side, with the US potentially hitting zero to negative net migration for the first time since the 1930s4, construction labor is likely to see strain.

M&A Market Implications

The M&A market today is incredibly bifurcated – most defensive sectors are risk-on and many cyclical areas are risk-off. Companies with exposure to the uncertain outlook for tariffs, inflation, and consumers are in a difficult position right now, as buyers are less willing to make major bets on exactly what the future looks like. However, markets that are relatively insulated from these factors are being chased by PE firms and strategics. That’s creating an avalanche of money, all chasing these opportunities, as groups can use the factors noted above to develop a long-term thesis with fewer uncertainties.

For our clients, our bet would be continuing to lean into capital budgets of utilities. Pockets of opportunity continue to exist, but thorough analysis of specific opportunity is needed vs. pushing for broad exposure to utilities, as these markets will continue to evolve. Bets exclusively on AI feel overvalued today based on our risk lens, but bets on the increases in electricity consumption and grid hardening have clear long-term demand drivers. As noted previously, nearly every major PE shop has a thesis around utility services, and strategics have long-term demand in their sights. Due to elevating multiples for these businesses, buyers need to extract value in order to make compelling ROI, but “priced to perfection” likely won’t result in achieving target returns.